The 2026 tariff landscape for golf bags is more challenging than ever, with rising costs impacting manufacturers, importers, and retailers. Here’s what you need to know:

- U.S. Tariffs: A baseline 10% tariff applies to most imports. Products from China face additional duties, with golf bags made of man-made fibers taxed at a total of 52.6%. Vietnam and Taiwan offer lower rates at 10%, making them attractive sourcing options.

- EU Changes: The EU now requires 10-digit TARIC codes for customs clearance, and a flat €3 duty per tariff sub-heading will apply starting July 1, 2026.

- Asia’s Role: Vietnam and Taiwan are gaining ground as cost-effective production hubs, while China faces high tariffs and increased competition.

- Cost Recovery: U.S. importers can claim refunds on tariffs paid under invalidated IEEPA duties, with a five-year window for retroactive claims.

- Oil Prices Impact: Shipping costs are up due to geopolitical tensions, further affecting supply chains.

Key takeaway: Businesses must monitor tariff changes, refine sourcing strategies, and explore cost-saving measures like duty drawback programs to stay competitive in this evolving market.

US Tariff Classifications and Rates for Golf Bags

HS Code 4202.92 Explained

When golf bags are imported into the United States, they are typically classified under HS Code 4202.92, particularly if they have a textile or plastic surface. This classification stems from Chapter 95’s exclusions, which specifically state that sports bags falling under heading 42.02 are not considered sports equipment.

The United States uses a 10-digit HTS (Harmonized Tariff Schedule) system, where the first six digits align with global standards, and the last four digits determine the applicable duty rate. Material composition plays a key role here – golf bags made from man-made fibers like nylon or polyester are categorized differently than those made from cotton, resulting in varied duty rates.

"Customs compliance is not optional overhead. It is a direct cost center that affects your landed cost, your delivery timelines, and your margin on every imported SKU."

– Siddharth Sharma, Strategy Lead, Nventory US

Errors in classification can lead to severe financial penalties, ranging from 20% of the dutiable value to as much as four times the lawful duties. Considering that US Customs and Border Protection processes around 33 million import entries annually, ensuring accurate classification is not just important – it’s essential.

Looking ahead, the tariff landscape becomes even more complex with the 2026 revisions, particularly for goods originating from China.

2026 Updates to US Tariff Rates

The updated 2026 tariff revisions emphasize the importance of accurate classifications, as they directly influence duty costs. The 2026 HTS Revision 1, issued by the United States International Trade Commission on January 15, 2026, provides the latest framework for tariff classifications. For golf bags imported from China, the duty structure includes additional Section 301 tariffs.

For sports bags under HS Code 4202.92, the MFN (Most-Favored-Nation) base rate is 17.6%. However, products from China face extra charges. For instance, general sports bags classified under 4202.92.91 incur a total duty rate of 27.6%, which combines the 17.6% base rate with a 10% surcharge under heading 9903.03.01.

Golf bags made from man-made fibers under HTS 4202.92.31 are subject to even higher rates, with a total effective duty of 52.6%. This includes the 17.6% base rate, a 25% Section 301 duty (9903.88.03), and a 10% surcharge (9903.03.01). Such distinctions based on material composition can result in a 25% difference in total duty costs.

| HTS Code | Description | MFN Base Rate | China Total Rate |

|---|---|---|---|

| 4202.92.15 | Sports bags of cotton | 6.3% | 16.3% |

| 4202.92.31 | Sports bags of man-made fibers | 17.6% | 52.6% |

| 4202.92.91 | Other sports bags (man-made fibers) | 17.6% | 27.6% |

For companies like Keep Perfect Golf, which specializes in custom golf bags made from various materials, understanding these tariff differences is crucial. Confirming the material composition before shipment can help avoid unexpected duty costs that could impact profit margins. Additionally, importers should keep an eye on potential exemptions under Section 301 headings 9903.88.13 through 9903.88.69, which might provide relief for certain products.

sbb-itb-4fa7e8b

EU Tariff Changes for Golf Bag Imports

The European Union has updated its tariff framework for 2026 through Commission Implementing Regulation (EU) 2025/1926, which was published on October 31, 2025. These changes to the Combined Nomenclature (CN) and Common Customs Tariff officially took effect on January 1, 2026. Golf bags imported into the EU are now classified under HS Code 9506.39, which includes golf bags and similar cases. It’s worth noting that the U.S. classifications differ, as they rely on material composition. These updates represent a notable shift from earlier practices, requiring importers to quickly adapt.

A major change comes into play on July 1, 2026, when the EU eliminates the low-value import exemption for shipments under €150. Instead, a flat €3 customs duty will apply per tariff sub-heading. For instance, if a shipment contains golf bags along with items from two other tariff categories, the total duty would be €9 (€3 per category). This adjustment is expected to impact businesses handling multi-category shipments.

Another critical update is the requirement for businesses to use 10-digit TARIC codes for customs clearance instead of the simpler 6-digit HS codes. Currently, 30–40% of tariff codes in declarations are reported as incorrect, which can lead to audits and delays at customs. As Adnan Zaheer, CEO of iCustoms, highlights:

"The effectiveness of customs today is directly tied to the quality of its digital intelligence – structured data, early risk signals, and systems that connect authorities and operators in real time".

In addition to these centralized changes, individual EU member states are introducing their own handling fees. For example, Romania has added a national fee of approximately €5 (25 lei) per package starting January 1, 2026. France followed with a €2 mandatory handling fee per item line as of March 1, 2026. Similarly, Italy and the Netherlands are planning to implement their own €2 fees later in 2026. These fees, when combined with the €3 customs duty, could significantly increase the landed cost for businesses like Keep Perfect Golf, especially for smaller shipments of custom golf bags.

The 2026 CN edition also introduced 27 new codes and either removed or redefined 13 codes. To avoid issues, businesses should review and update their master data to align with the 2026 CN edition well ahead of the EU Customs Data Hub launch in 2028. These changes highlight the importance of revising tariff strategies to stay compliant and manage costs effectively.

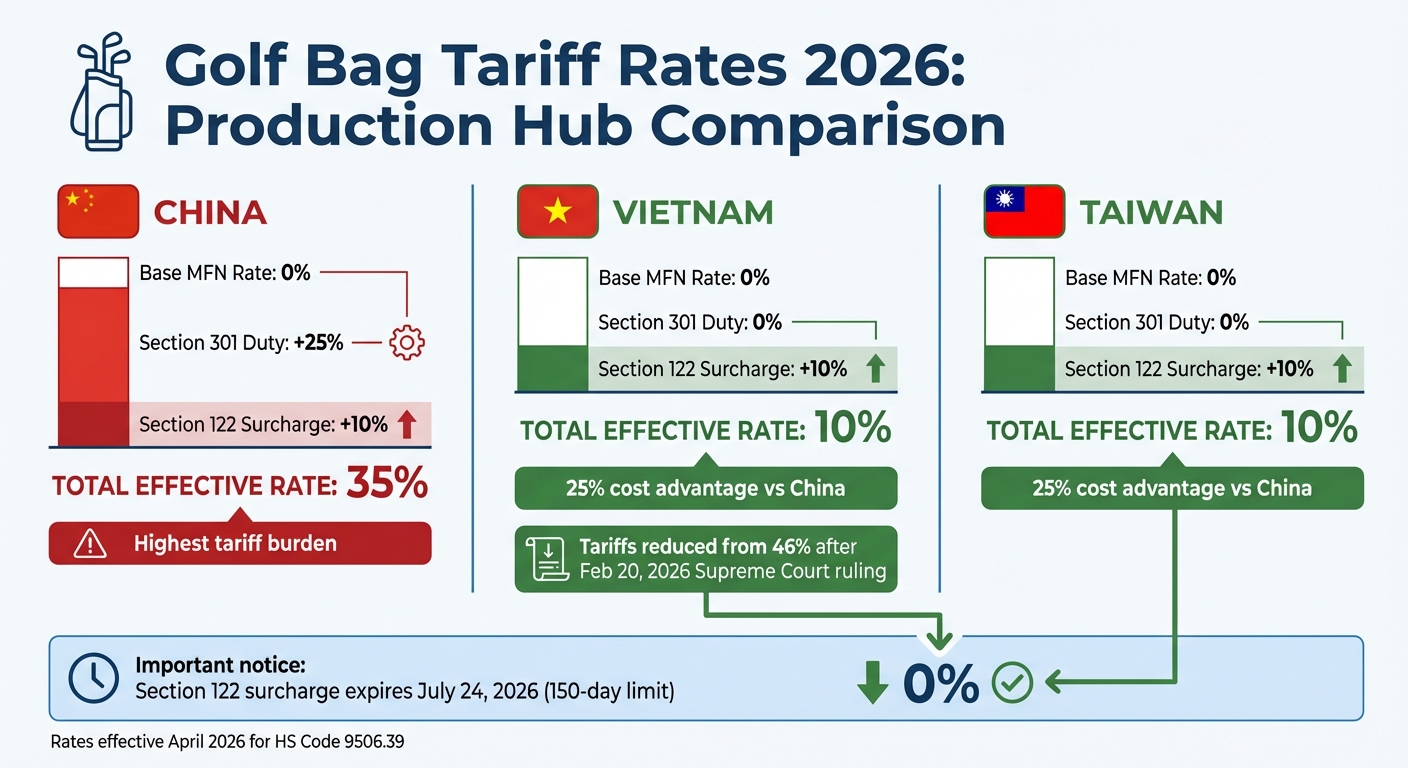

Asian Production Hubs: Tariff Structures in China, Vietnam, and Taiwan

2026 Golf Bag Tariff Rates Comparison: China vs Vietnam vs Taiwan

China’s Export Tariffs for Golf Bags

China continues to dominate as a major golf bag manufacturer, but its tariff landscape has become more challenging. Since April 2026, golf bags classified under HS Code 9506.39 are subject to a layered tariff system when imported into the U.S. This includes a base rate, Section 301 duties of 25%, and an additional Section 122 global surcharge of 10%. Together, these add up to a 35% effective tariff rate for Chinese-made golf bags.

This cumulative structure complicates cost calculations. The Section 301 duties, which specifically target Chinese imports, significantly widen the cost disparity between China and other production hubs. Adding to this, the $800 de minimis exemption was eliminated in 2025, meaning even small sample shipments are now fully taxed.

These changes have prompted many businesses to explore alternative sourcing options with lower tariff burdens.

Vietnam and Taiwan: Tariff Advantages

Vietnam and Taiwan have become strong contenders for golf bag production, offering a noticeable tariff advantage over China. Both countries are only subject to the 10% Section 122 surcharge when exporting golf bags to the U.S., resulting in a 25% cost advantage compared to Chinese products. This is because neither Vietnam nor Taiwan is impacted by the Section 301 duties.

A key development occurred on February 20, 2026, when the Supreme Court overturned IEEPA-based reciprocal tariffs on Vietnam. Before this ruling, Vietnam faced tariffs as high as 46%, but the decision reduced the rate to just 10%, reestablishing Vietnam as a top "China+1" manufacturing option. Taiwan enjoys the same reduced tariff structure.

The Section 122 surcharge has a statutory limit of 150 days, set to expire around July 24, 2026, unless Congress decides to extend it. If it is not renewed, imports from Vietnam and Taiwan could revert to MFN-only rates, potentially eliminating the 10% surcharge altogether. For companies like Keep Perfect Golf, which specialize in custom golf bag manufacturing, this creates opportunities but also introduces uncertainty in planning sourcing strategies.

Tariff Rate Comparison Table

Here’s a breakdown of the current tariff rates for golf bags across the three major production hubs:

| Country | Base MFN Rate (HTS 9506.39) | Section 301 Duty | Section 122 Surcharge | Total Effective Rate (April 2026) |

|---|---|---|---|---|

| China | 0% | 25% | 10% | 35% |

| Vietnam | 0% | 0% | 10% | 10% |

| Taiwan | 0% | 0% | 10% | 10% |

Note: Section 122 tariffs are set to expire around July 24, 2026.

Additional Cost Considerations

Tariffs aren’t the only factor impacting costs. As of April 12, 2026, a U.S. naval blockade of the Strait of Hormuz has driven Brent Crude oil prices to $118 per barrel, causing shipping costs to surge. Transit times have also increased by 10–15 days, adding another layer of complexity to supply chain planning. These external factors further influence the overall cost-effectiveness of sourcing from Asian production hubs.

Tariffs in India and Southeast Asia

As production hubs across Asia adjust their tariff policies, India and Southeast Asia are refining their trade frameworks to remain competitive in a changing global market. India, in particular, is reshaping its role in the golf bag supply chain by rapidly expanding trade agreements. On February 7, 2026, the U.S. lifted a 25% sanctions-based tariff on Indian goods and replaced it with a focused 18% reciprocal tariff on textiles and leather used in golf bag production. While this move shifts from broad sanctions to specific product-based duties, it still presents cost challenges for manufacturers, albeit within a more predictable framework.

India’s Free Trade Agreement (FTA) network is also growing steadily. The India-EFTA TEPA, which went into effect on October 1, 2025, now covers 100% of non-agricultural products, including golf bags classified under HS Code 9506.39. Additionally, the India-EU FTA, finalized on January 27, 2026, will eliminate tariffs on 86% of India’s tariff lines, accounting for 93% of trade value, once ratified. India is also revisiting agreements with ASEAN and South Korea to expand trade liberalization and update duty structures. These agreements are expected to simplify imports and strengthen supply chain strategies across the region.

India’s Union Budget 2026-27 and new digital customs initiatives are further streamlining tariff structures, which directly affect landed costs. Starting May 1, 2026, these reforms aim to address duty inversions and improve classification systems. Importers should carefully review their Basic Customs Duty assumptions, as exemptions have been removed in favor of supporting domestic production. The introduction of the Air Suvidha platform has also digitized customs declarations, cutting clearance times at major airports by an estimated 30%.

Currently, India ranks as the third-largest supplier of golf bags by quantity, shipping 1,119,209 units this year. This highlights India’s growing importance as both a key market and an emerging manufacturing hub. Similarly, Vietnam and Indonesia are becoming increasingly attractive sourcing destinations due to stable tariff policies and shifting trade dynamics. As India’s FTA network continues to develop and tariff structures stabilize, manufacturers must carefully confirm whether their shipments qualify for preferential origin status under these agreements before calculating landed costs.

Supply Chain Strategies and Tariff Refunds for 2026

With tariff classifications constantly evolving, refining supply chain strategies has become essential for managing rising costs.

Importers have the opportunity to recover up to 99% of paid tariffs through duty drawback programs when golf bags are exported, used in manufacturing for export, or destroyed. Shockingly, around $15 billion in U.S. duty drawback refunds go unclaimed annually. These programs allow businesses to retroactively claim refunds on entries dating back to 2021, thanks to the five-year window from the date of importation.

Substitution and Manufacturing Drawbacks

Under substitution drawback (19 U.S.C. § 1313(j)), companies can match exports with different imports as long as both share the same 8-digit HTS code (e.g., 4202.92 for golf bags) and are deemed commercially interchangeable. This removes the need to track specific imported items. Meanwhile, manufacturing drawback applies when imported components, like specialized fabrics or frames, are used to manufacture golf bags in the U.S. for export. However, it’s important to note that Section 232 duties and antidumping/countervailing duties are not eligible for drawback. These mechanisms work in tandem with broader supply chain strategies to maximize cost recovery.

Tariff Refunds After IEEPA Ruling

A Supreme Court ruling on February 20, 2026, invalidated tariffs imposed under the International Emergency Economic Powers Act (IEEPA). As a result, duties paid since 2025 became recoverable. To streamline the refund process, U.S. Customs and Border Protection (CBP) introduced the Consolidated Administration and Processing of Entries (CAPE) system within the ACE platform. Starting February 6, 2026, all duty refunds are now issued exclusively via electronic ACH transfer. Importers must register their ACH details through the ACE Portal to ensure they receive refunds; failing to do so could result in claim rejection.

Free Trade Zones, Bonded Warehouses, and the First Sale Rule

Free Trade Zones (FTZs) offer another cost-saving option by allowing imported components to be used in manufacturing without paying duties upfront. If the finished product is exported, no duty is ever owed.

"If the manufactured item is exported outside the U.S., no duty is ever due", explains Lauren Pittelli, Founder and Principal at Baker Logistics Consulting Services.

For high-value inventory, bonded warehouses enable deferred duty payments, offering additional flexibility. The First Sale Rule provides another cost-cutting strategy by allowing importers to declare goods based on the "first sale" price in a multi-tiered supply chain, reducing the dutiable amount significantly.

Automation and USMCA Considerations

AI-powered platforms are revolutionizing tariff recovery by automating HTS code audits and reviewing historical entries. These tools uncover 15–20% more refunds compared to manual methods. To expedite refunds, companies should conduct lookback audits of their past five years of import entries and apply for CBP privileges like "Accelerated Payment" and "Waiver of Prior Notice", which can reduce refund timelines from years to weeks.

Under the USMCA agreement, qualifying products from Canada and Mexico are exempt from the 10% Section 122 global tariffs introduced in February 2026. However, substitution drawback is generally not allowed for exports to these countries.

Golf Bag Tariff Projections Through 2030

The tariff outlook for golf bags is shaping up to be increasingly unpredictable through 2030, thanks to shifting trade policies and geopolitical tensions. The trade-weighted average tariff on manufactured goods surged from 1.9% in 2024 to 4.7% in 2025. For golf bag manufacturers and importers, this marks a significant shift in costs compared to just a couple of years ago. These changes signal further market adjustments in the years ahead.

Different production hubs are experiencing vastly different tariff rates. By 2025, China is projected to face a staggering 104% reciprocal tariff rate, while Vietnam’s stands at 46%, Taiwan at 32%, and South Korea at 25%. These rates are in addition to the baseline global tariff of 10%. However, these figures are far from stable, as they remain subject to ongoing trade negotiations. Vietnam, for instance, has been actively working to lower its tariff rates through diplomatic efforts.

The financial strain on manufacturers is already evident. Higher tariffs have driven up retail prices significantly, forcing companies to adapt. Strategies include redesigning products to minimize dutiable components, restructuring supply chains to use countries like Mexico for final assembly, and even implementing mid-season price hikes to offset tariff costs.

Despite these challenges, the golf bag market is still growing. By 2030, it is expected to reach $2,323.8 million, with a compound annual growth rate (CAGR) of 9.5%. This growth is fueled by the rising number of registered golfers, which jumped from 3.1 million in 2021 to 8.0 million in 2023.

Looking ahead, businesses must also prepare for new environmental and trade-related challenges. Carbon pricing and stricter green regulations are likely to influence trade policies, potentially leading to preferential treatment for eco-friendly golf bags made from recycled or bio-based materials. Additionally, trade patterns are shifting, with "South-South" trade corridors gaining prominence – 57% of exports from developing countries are expected to flow to other developing markets by 2026. Companies that diversify their sourcing strategies and adapt to environmental compliance requirements will be better equipped to navigate this turbulent tariff landscape.

Conclusion

The 2026 tariff landscape for golf bags requires businesses to act quickly and make informed decisions to adapt to new challenges. The shift from IEEPA tariffs to a temporary 10% Section 122 surcharge, effective February 24, 2026, opens up a 150-day window before new Section 301 or 232 duties come into play. For major manufacturers like Callaway, these changes bring immediate financial implications.

Prioritize claiming refunds. The Supreme Court’s ruling on February 20, 2026, struck down IEEPA tariffs, unlocking access to approximately $166 billion in refunds across over 53 million entries. To streamline this process, U.S. Customs and Border Protection will introduce the CAPE system in late April 2026, enabling electronic claims via ACH. Businesses must act now by verifying ACE portal access, setting up ACH payment details, and preparing entry summary data in CSV format. Securing these refunds not only offsets financial strain but also sets the stage for rethinking sourcing strategies.

Strategic sourcing is the next key step. New trade agreements are opening opportunities for lower tariff rates. For example, the EU-India FTA eliminates tariffs on 96.6% of goods, including textiles and leather – materials commonly used in golf bags. Similarly, the U.S.-Taiwan deal caps reciprocal tariffs at 15%. Companies that diversify production to these regions, while maintaining assembly in areas like Mexico, can significantly reduce tariff costs.

Leverage technology for compliance and efficiency. Real-time data tools and AI-driven systems for tariff classification and duty calculation are becoming indispensable. Properly classifying products under HS Codes – such as golf bags under 9506.39 instead of general containers under 4202.92 – can result in notable duty savings. Staying ahead of policy changes with these tools ensures smoother operations.

For manufacturers and importers like Keep Perfect Golf Gear (https://keepperfectgolf.com), which focuses on OEM/ODM production and global delivery, staying informed about these tariff trends is critical. By taking these steps – securing refunds, optimizing sourcing strategies, and adopting advanced compliance tools – companies like Keep Perfect Golf Gear can not only navigate the 2026 tariff shifts but also strengthen their position for future changes.

FAQs

How do I pick the right HTS/HS code for my golf bags?

To choose the right HTS/HS code for your golf bags, pay close attention to the material and construction of the product. For golf bags made of leather or similar materials, the applicable HS Code is usually 42029110. On the other hand, bags crafted from synthetic fabrics like nylon or polyester fall under different classifications. Make sure to carefully document the materials used and match your product’s details with the tariff definitions. Misclassification can result in delays, penalties, or increased costs, so accuracy is key.

What’s the fastest way to claim 2025–2026 U.S. tariff refunds?

The fastest route to secure U.S. tariff refunds for 2025–2026 is through Customs and Border Protection’s (CBP) upcoming automated refund process on the ACE platform. This system is set to roll out in approximately 45 days. Once it’s live, make sure to file the required declarations promptly to simplify and expedite your refund claims.

Should I shift production from China to Vietnam or Taiwan in 2026?

Shifting golf bag production from China to Vietnam or Taiwan in 2026 could help cut costs, largely due to differences in tariffs. Currently, golf bags made in China are subject to tariffs ranging from 22.5% to over 65%, while Vietnam offers a lower tariff rate of about 15%. Taiwan might also provide cost savings, especially with potential changes in tariffs and geopolitical factors.

However, before making a decision, it’s important to weigh additional factors like lead times, the quality and availability of production infrastructure, and how golf bags are classified under specific tariff codes. These elements could significantly impact the overall cost and efficiency of production.